Physician Compensation 2011: How Much am I Worth?

by Bruce Maller; Robin Blackstone, MD, FACS, FASMBS; and Jaime Ponce, MD, FACS, FASMBS

Author affiliation: Bruce S. Maller is President and CEO of BSM Consulting™, an internationally recognized healthcare consulting firm. For more information on BSM Consulting, visit www.bsmconsulting.com. Dr. Blackstone is President-Elect of the American Society for Metabolic and Bariatric Surgery and Medical Director, Scottsdale Healthcare Bariatric Center, Scottsdale, Arizona. Dr. Ponce is the Chair of the ASMBS Insurance Committee and Medical Director of Hamilton Medical Center Bariatric Program, Dalton, Georgia.

Financial disclosure: Mr. Maller is President of BSM Consulting, a company that provides fee-based consulting services to physician practices. Drs. Blackstone and Ponce report no conflicts of interest relevant to the content of this article.

Bariatric Times. 2011;8(5):24–28

Abstract

Many surgeons who have worked for themselves are now facing increasing pressure either from internal forces (e.g., family, stress of running their own business) or external forces (e.g., facility, government regulation) to merge their practice with one of the facilities in which they work. This article is a preview of a special course on physician compensation, coding, and reimbursement that the American Society for Metabolic and Bariatric Surgery will feature at their 28th annual meeting, in Orlando, Florida, in June of 2011.

Introduction

Why has there been a trend from private practice to hospital-based practice models? The answer is pretty simple. The business model of bariatric surgery makes it very difficult for a private practitioner to meet the needs of patients while also maintaining reasonable operating margins. In most cases, less than 10 percent of the total fee charged for bariatric surgery ends up on the professional fee side of the equation. The vast majority of the money ends up on the facility side of the ledger.

This challenge is brought to light when one considers the myriad of preoperative requirements imposed by third-party payers. Assuming the patient even has insurance that will pay for the procedure, there are many hurdles that have to be overcome, which require answers to the following:

1. Is there an active bariatric surgery benefit?

2. What are the payer requirements for bariatric surgery authorization?

These will typically include:

a. Quality related considerations such as such as an American Society for Metabolic and Bariatric Surgery Center of Excellence (ASMBS COE) or a proprietary designation like Blue Cross/Blue Shield Centers of Distinction (COD)

b. Financial concerns, including deductible, copay, and benefit design issues

c. Presurgical requirements that may otherwise be imposed by the payer, the most common of which include a mental health examination, medically supervised weight loss requirements, a dietary evaluation, as well as documentation of a history of obesity

3. Assisting patients in navigating the reimbursement process

4. Submission of the required paperwork for preauthorization

5. Dealing with a possible denial and helping a patient with the associated appeal process.

Many physicians have found it to be simply untenable to assist patients in this complex process without the support of an affiliated hospital or surgical facility.

Providing any level of support from hospitals to private practitioners can be compromised due to the implications of federal and state regulations that limit the ability of hospitals and physicians to share income or resources without running afoul of the self-referral or anti-kickback statutes. To some degree, these concerns can be mitigated if a physician becomes an employee of the hospital.

There are few, if any, other medical procedures that require the same number of medical professionals in the care continuum in order to enable patients to achieve optimal outcomes. In some cases, a bariatric surgery patient may “touch” as many as 5 to 10 medical professionals before they ever reach the operating room table.

Clearly, to expect the private practitioner with limited resources to be able to triage and manage the care of these patients is a daunting task. The economic and clinical challenges associated with managing bariatric surgery patients are clearly the driving forces behind the trend toward the integration of physicians with hospital systems.

So, what is my practice worth?

Assuming a practitioner decides to sell his or her practice to a hospital, it is fair to ask, “What is my practice worth?” In some cases, the physician has limited or no negotiating leverage, is at the mercy of the hospital, and may find very little opportunity to monetize the value of his or her practice in a satisfactory manner. In these cases, one may simply be offered an employment contract with nominal consideration for the hard assets of the practice. In other cases, the practitioner may bring greater value to the table and also have some negotiating leverage, assuming there is more than one potential buyer or strategic partner. One’s negotiating position is enhanced to the extent the physician or practice has strong name recognition, a robust infrastructure, and “institutional” value in the market.

Ordinarily, the value of a business is a function of its income-producing capacity. It is important for the physician to look at the transaction from the standpoint of the buyer and ask how the buyer will extract value from the practice following a sale. A buyer will generally have an expectation of receiving a market-based return on investment (ROI). For transactions of this nature, buyers normally expect to receive an annual “cash on cash” return in the range of 25 to 40 percent. The buyer will ordinarily complete a forecast of future revenue and operating costs in order to evaluate the overall financial impact of the proposed transaction, including the potential ROI. This analysis is often completed in order to assess what a buyer might be willing to pay for the practice.

In arriving at a determination of value, the parties may agree to hire a third-party appraiser to place a value on the business. The appraiser will often use three valuation methods; however, when it comes to determining the existence of goodwill, the appraiser will use a market-based approach or the discounted-cash-flow method of valuation. With the market-based approach, the appraiser will look at similar transactions. This can be challenging since most transactions are private and, as such, information on details of the sale are not readily available in the public domain. The appraiser is then left to look at similar transactions in the public domain and then extrapolate a “market multiple” that takes into account other relevant factors.

The discounted-cash-flow method requires the appraiser to make several assumptions about future revenue and expenses as well as expected rates of return on future earnings. One obvious challenge in this instance is whether the selling physician gets any “credit” for the downstream cash flow opportunities available to the hospital. Ordinarily, this value is considered outside the scope of the appraiser’s report.

From the seller’s perspective, the value of a practice normally comprises the following three elements:

1. The value of the hard assets. Hard assets include leasehold improvements, furnishings, fixtures, and equipment deployed in the practice. The value of these assets is normally determined by use of a third-party appraisal. Whether any value is assigned to the leasehold improvements will be a function of whether the purchasing entity will retain the practice at its current location and whether the selling physician actually made the capital investment in these assets.

2. The value of collectible accounts receivable (A/R). It is most common for the selling physician to retain his or her A/R at the time of closing, and as such, they are not included in the selling price.

3. The income-producing value or goodwill of the practice. As noted, goodwill value is normally more difficult to assess since there is not a textbook formula or rule of thumb that can be applied. Most purchasers will look at the numbers and attempt to determine a potential ROI after subtracting all costs from forecasted revenues. Assuming the selling physician will become an employee of the hospital, the compensation package of the physician will be considered a part of overhead in evaluating potential profits.

There are many business, tax, and legal considerations that need to be considered in arriving at the fair market value of the practice. In addition, there can be limitations on the amount of consideration that may be paid by a nonprofit institution versus a for-profit facility. It is strongly advised that surgeons retain legal and tax advisors that are experienced in these matters. It is also important to point out that transactions between physicians and hospital systems also need to be considered within the context of Stark Laws as well as the Anti-Kickback Statutes.

Physician Self-Referral Law. The Physician Self-Referral Law, commonly referred to as the Stark Law, prohibits physicians from referring patients to receive “designated health services” payable by Medicare or Medicaid from entities with which the physician or an immediate family member has a financial relationship unless an exception applies. Financial relationships include both ownership/investment interests and compensation arrangements.

Anti-Kickback Statute. The Anti-Kickback Statute prohibits the knowing and willful payment of “remuneration” to induce or reward patient referrals or the generation of business involving any item or service payable by the federal healthcare programs (i.e. Medicare and Medicaid). Each party’s intent is a key determinant in assessing liability under the statute.

There are Safe Harbor provisions that protect certain payment and business practices that could otherwise implicate this statute. To be protected by a Safe Harbor, the arrangement must fit all of its requirements. One Safe Harbor that is important in physician-hospital sale transactions “protects” payments that are made to bona-fide employees. Although it is beyond the scope of this article to focus on this important issue, this Safe Harbor provides that the term remuneration, as used in the statute, does not include any amount paid by an employer to an employee, assuming there is a bona-fide employment relationship.

A hospital buyer may have strategic reasons for the acquisition; however, it is uncommon that a board or senior management team will recommend or approve any transaction unless there is a financial rationale for the purchase. Of course, one important consideration for the buyer is whether the facility has an existing bariatric service line or see the acquisition as an opportunity to get into the business. This factor will often be a key factor that impacts a seller’s leverage and negotiating position.

Compensation Models in Hospital-Based Employment Agreements

The following are the three basic compensation models commonly seen in hospital-physician relationships:

Base pay/straight salary. As the name implies, the physician will receive a fixed salary normally stated in annual terms with payment made in accordance with the normal payroll cycle of the employer. The pay is normally determined based on several factors, including historical pay level of the physician, comparable pay with other like-kind surgeons with similar background and experience, industry salary surveys, and/or the pay structure of the hospital medical staff. Normally, this type of pay structure will not include any type of incentive bonus.

Base pay plus incentive. As the name implies, this structure will include a combination of a fixed salary plus incentive. The salary component is determined using the same factors noted previously. Ordinarily, the salary will be in the range of 60 to 80 percent of total compensation. The incentive is normally tied to individual production metrics, such as collections, patient visits, surgical cases, or relative value units (RVUs). Normally, there is a production threshold following which the physician is entitled to a certain payout for excess production.

In some cases, incentive criteria may include quality of care or patient satisfaction measures. These tend to be less popular given the inherent challenges in providing objective measures that tie directly to one’s productivity. In addition, some models also provide additional compensation for administrative duties or “citizenship” time invested by the physician. The latter would include compensation for directorship or department leadership positions or other time invested to promote or support the facility.

Table 1 is an example of an incentive pay formula. In most cases, the incentive is calculated and paid on an annual basis; however, in some instances, incentive amounts are paid as earned over the course of the year.

In some instances, the physician or department is treated as a separate profit center and any compensation paid is treated as an expense against department revenue. With this approach, at the end of the fiscal year, department profits (or some percentage thereof) are normally distributed to the physician(s). This approach can be a bit tricky since the hospital may charge back certain indirect overhead expenses that may serve to artificially reduce department profits. Table 2 is an example of a profit center-based model.

Production-based model. In a production-only system, the physician receives compensation tied directly to an agreed-upon measure. One of the more common models is to pay out a percentage of professional fees collected on account of professional services provided by the physician. The use of work relative value units (wRVU) as a measure of production has also become increasingly popular. In large part this is due to the fact that work RVUs eliminate arguments about billing, collections, and fee schedules.

Background on Relative Value Units (RVUs)

Given their increasing popularity, it is important to provide some background on RVUs. When Medicare introduced the Resource-Based Relative Value Scale (RBRVS) in the early 1990s, unit values were assigned to each of 7,000 CPT codes. Each current procedural terminology (CPT) code was assigned three unit values—work, overhead, and malpractice. The work component was designed to include the physician’s time, skill level, training, and intensity of effort to provide a given service. A similar exercise was required for the overhead and malpractice components so, in the end, each CPT code is assigned a numeric value. For example, a new patient level-three office visit (99203) will have a lower number of units assigned than a complicated surgical procedure, such as gastric bypass.

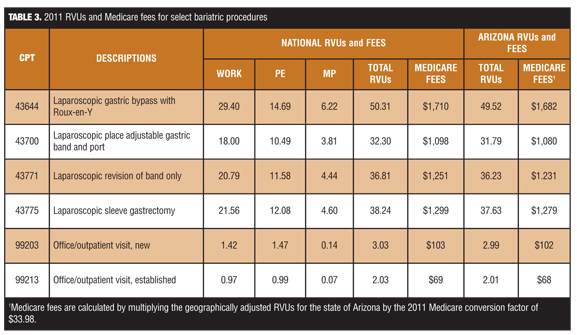

These values are geographically adjusted to reflect the cost of living and other factors. The geographically adjusted RVUs are then multiplied by a conversion factor (CF) in order to arrive at a local fee (for Medicare patients). Table 3 provides a list of the more common CPT codes used in bariatric surgery along with a breakdown of national RVUs as well as geographically adjusted RVUs for the state of Arizona.

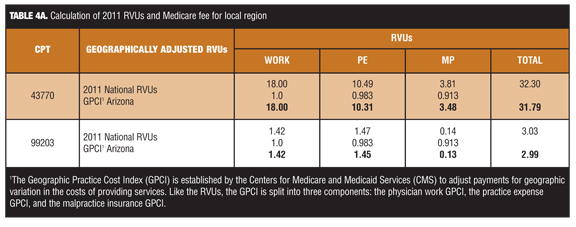

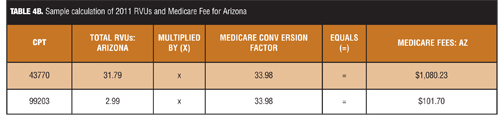

Most hospitals that use RVUs as a measure of production for compensation purposes focus only on the work RVUs. However, in order to maximize negotiating leverage, it is essential for physicians to understand the big picture. When the hospital uses a conversion factor it is critically important to understand the different factors that can come into play. For example, the 2011 national Medicare conversion factor is $33.98 (down from the 2010 level of $36.87). This amount is multiplied by the geographically adjusted RVUs in order to arrive at local Medicare payment rates for each covered service.Table 4a and Table 4b illustrate how each RVU component is adjusted in order to arrive at a local fee. Please note, for purposes of computing fees for a given locale, there are 89 different regions across the country.

Review of Industry Compensation Surveys

Physicians can easily evaluate their collection and compensation efficiencies by comparing professional collections in relationship to the number of associated RVUs generated in a given reporting period.

This can be illustrated based on a review of the Medical Group Management Association (MGMA) 2010 Physician Compensation and Production Survey (2010 report based on 2009 data).[2] The survey results indicate that the median compensation level for “hospital owned” general surgeons was $339,700. This was based on 495 respondents. Although there were only 24 bariatric surgeon respondents, the median compensation level was $355,916.

The median number of total RVUs produced was 12,422 for general surgeons and 10,884 for bariatric surgeons in the survey. If one divides the total compensation by the total RVUs, the compensation rate per RVU was $27.35 and $32.70, respectively.

According to the same survey, the median number of wRVUs generated was 6,908 for general surgeons and 8,047 for bariatric surgeons in the survey. By dividing the median compensation level by the wRVUs would indicate the pay rate was $49.17 and $44.22, per wRVU respectively.

Surveys also point out that higher-earning, hospital-based physicians can, in some instances, generate compensation in excess of total collected production or higher than the Medicare CF per total RVU. This partly due to the fact that hospitals generate income from facility fees and other sources that allow them to pay employed physicians additional amounts that are not otherwise tied to personal production.

It is important to also point out that the MGMA data are fairly consistent with results from the 2010 American Medical Group Association Compensation and Financial Survey,[3] which reported median compensation for general surgeons of $357,091, median wRVUs produced of 7,246, and a median pay rate per wRVU of $49.29.

Relative Value Unit Compensation Model

It is increasingly common for hospitals to compensate employed or contract physicians based on either total or work-related RVUs. In many cases, a base salary is provided that is tied to a targeted or budgeted number of RVUs. In addition to the base salary, the contract will typically include a provision that provides a payment rate per wRVU produced in excess of an agreed-upon threshold. The contract will normally include a provision such that if employment terminates prior to the expiration of a one-year term, the performance-based compensation is pro-rated. For example, if the physician completes six months of a one-year term, he or she would be eligible for 50 percent of the performance compensation.

The contract should also stipulate how RVUs are to be calculated. It is recommended that a schedule be appended to the contract that lists the relevant CPT codes as well as agreed-upon unit values. Additionally, the contract should include a provision that provides a mechanism to assign unit values to codes for which no RVUs may have otherwise been assigned. A simple method to do this is to compare the gross charge for the procedure with other “covered” procedures and assign the same or a similar number of work and/or total RVUs.

In some cases, the contract will provide a fixed sum per wRVU in excess of an agreed-upon threshold. In other cases the contract will provide for an increasing payment rate based on achieving higher levels of productivity.

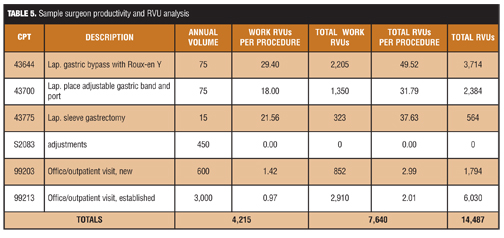

Table 5 provides a sample summary of productivity for a typical bariatric surgeon. The total RVUs produced during the reporting period was 14,487. At the same time, the number of wRVUs produced was 7,640.

Other Applications for RVUs

Hospitals use wRVUs not just in compensation planning but also in department budgeting. Physician base salaries may appear arbitrary; however, in most cases, the negotiated amounts have been reconciled within the context of individual provider or department budgets.

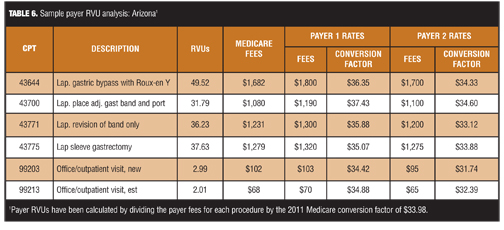

Reimbursement from other third-party payers is also impacted by RVUs. Today, the Medicare fee schedule has supplanted other relative value scales that were in use for many years. Third-party payers often base their reimbursement on a percentage of the local Medicare fee schedule. It is important that surgeons understand the use of RVUs in negotiating fee schedules with commercial plans. This should include a working knowledge of reimbursement rates and assigned relative value units to individual CPT codes. Table 6 provides an example sampling of third-party payers.

With the advent of healthcare reform, bariatric surgeons will need to better understand how delivery system changes will impact reimbursement and compensation models. The one constant is that more intimate knowledge of these systems will enable the surgeon to be in a more advantageous position at the bargaining table.

References

1. Centers for Medicare & Medicaid Services (CMS), HHS. Medicare program; payment policies under the physician fee schedule and other revisions to Part B for CY 2011. Final rule with comment period. Fed Regist. 2010;75(228):73169–860.

2. Medical Group Management Association, Physician Compensation and Production Survey, 2010 Report Based on 2009 Data. http://www.mgma.com

/physcomp/ Accessed April 28, 2011.

3. Compensation 2010: Emerging Models, Shifting Priorities, Persistent Demographics: Results from the AGMA 2010 Medical Group Compensation and Financial Survey by Bradley S.J. Vaudrey and Sara J. Loos, September 2010 Group Practice Journal. mcgladrey.com/pdf/amga_

survey_2010.pdf. Accessed April 28, 2011.

Category: Past Articles, Review

Subscribe

If you enjoyed this article, subscribe to receive more just like it.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}